PERSPECTIVES #4

Bridging the energy transition investment gap : the key role of SMEs and midcaps

Télécharger l’intégralité du document en PDFBridging the energy transition investment gap : the key role of SMEs and midcaps

Since the Paris Agreement, an even stronger focus is put on how we can collectively achieve decarbonization of the global economy and maintain temperature increase below 1.5°C. The energy sector is impacted more than any other sector, as it must totally overhaul its asset base and underlying design in the course of one or two decades.

The challenge is to a large extent unprecedented, given the magnitude of the transformation needed and more importantly the pace of this transformation, should we want to keep in check the consequences of climate change. IEA calls for a doubling of low-carbon power generation, energy efficiency and power grids yearly investments in its World Energy Investment 2019, from c. $900bn / year to c. $1,950bn / year.

The central question is then: how do we fill the investment gap? More precisely, which actors have the ability to answer such a massive investment need? In an excellent piece in the Financial Times, Nick Butler argued that public money was a central piece to channel investments contributing to the transition to a low carbon economy. But in a context of constrained sovereign budgets, it is unlikely states can play this role alone1. Our conviction is that Small and Medium Enterprises (SMEs) and midcaps are critical to bridging this gap.

We focus on Europe, which has been the pioneer in energy transition since the early 2000s and that set ambitious targets for 2030, and eventually wants to achieve a net-zero emissions economy by 2050.

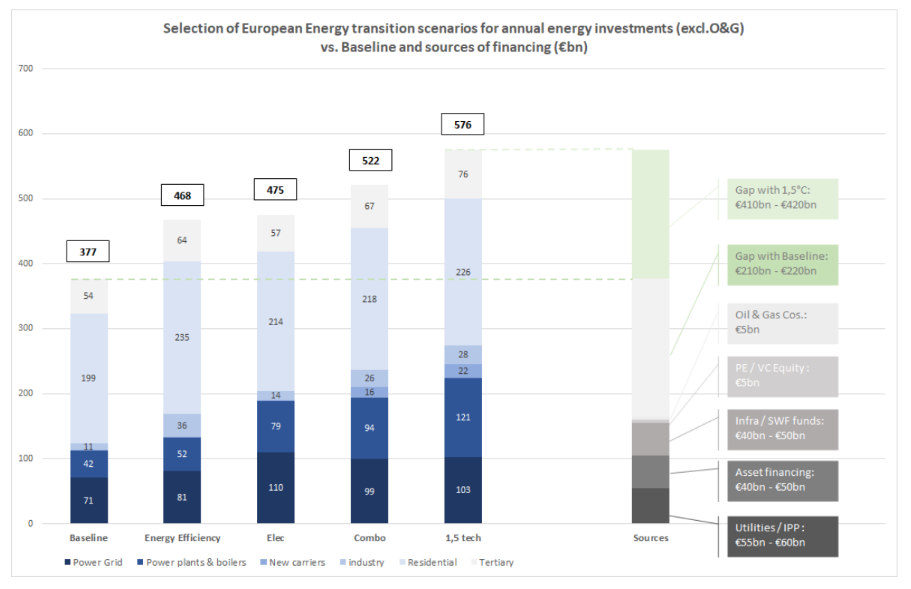

Source: TiLT Capital analysis; European Commission (Nov 2018) “In-depth analysis in support of the Commission communication”; Wood Mackenzie (Nov 2019) “Wood Mackenzie Breakfast Briefing: European Power & Renewables”; IEA (May 2019) “World Energy Investment”; Frankfurt School – UNEP – BNEF (2019) “Global trends in Renewable energy investments”; Preqin (July 2019) “Preqin markets in focus: Alternative assets in Europe”

The chart above attempts to propose a synthetic view of both the magnitude of the challenge in raw numbers, but also in terms of players strategy. The investment gap is obvious: whatever the scenario, even compared to its own baseline scenario aiming at respecting its 2030 targets, Europe lacks anywhere between €200bn and €400bn of investments per year. Currently, it invests merely around €160bn on an annual basis.

What this chart also underscores is that the investment capabilities of the historical players are far from sufficient. A quick review of these players may help better understand why SMEs and midcaps are key to this challenge.

Utilities have historically invested €55-60bn / year over the past five years. It is unlikely these companies will increase significantly their investment capabilities. As owners of the legacy assets of the energy system, they have been hit directly by the collapse of entry barriers and the disruption in energy markets. While they are critical to the system, they face the need to conduct their own transition, translating into tight financial equations (relatively high gearings and diminishing margins) and leaving little room for increased investment budgets.

Oil and Gas companies have recently entered the power sector in a more systematic way than they have in the past. They indeed come with significant investment and financing capabilities: Shell, for example, has generated $53bn of cash flow from operations and invested $14bn in 2018. Yet, the returns (and risks) associated with power investments differ quite materially from those of the oil and gas industry, and it is unlikely that investors will agree to see Oil and Gas companies move completely away from their historical business to invest massively in low carbon energy in the short term. It is hence improbable that these companies will contribute more than €10bn per year to energy transition investments in Europe.

Since the early 2010s, infrastructure funds and long-term investors such as sovereign wealth funds and pension funds have poured significant amounts of capital in the energy sector, under the form of own equity (roughly €40-50bn per year). Alongside banks, they have also channeled most of the annual €40-50bn asset financing (mostly project financings) in Europe, as a mean to protect and enhance their returns. But this pattern has been largely driven by the growth in renewable energy investment, supported by tariffs that gave attractive risk-return profiles with long-term, stable yield. But in order to achieve the energy transition, a different type of capital is needed, with an ability to take different risks and be more on the industrial side. Public support spreads across these various players, either through loans, equity or guarantees. Several initiatives have already emerged to tackle this issue, one of the most prominent being the European Investment Bank (EIB) revision of its climate ambition. By committing to devote 50% of its resources to environmental sustainability and the fight against climate change, the EIB wishes to support and trigger over €1,000bn of investment in this sector in the decade 2021-2030.

Part of the public support will also be directed towards the residential segment, under the form of regulations, subsidies and incentives, as well as tax policies and regulations in favor of energy transition. As “residential” investment need amounts to roughly €200bn per year under any scenario, it will be key that European states find the means to channel money to that sector while ensuring that the burden of cost is acceptable to the population. This ambition is written in gold letters in the Clean Energy for All package, but the policies to achieve this ambition are yet to be fully designed2.

Eventually, faced with this finding, support to SMEs and midcaps appears to be the most promising way in bridging this gap. In Europe, there are 1.65 million SMEs with more than €2m turnover, representing a cumulated value added in 2017 of €2,600bn3. If only 5% of these small companies invest each year €1m, that would be €80bn channeled to energy transition investments.

The role of these players is magnified by the collapse of entry barriers of the energy sectors, due to three major changes:

- Energy production is accessible with relatively low capital requirements. Even consumers can become energy producers (the now famous “prosumers”);

- Demand management and energy efficiency becomes a point of focus for a number of clients (residential or commercial and industrial), opening up businesses for smaller companies able to provide expertise and services in these fields;

- Power market designs go towards lower granularity (focusing on more local levels and real time patterns), increasing the demand for tailor-made expertise and solutions.

As energy transition percolates in all sectors of the economy (from manufacturing to logistics to real estate), energy challenges will need to be tackled by companies who not only know energy, but also who understand the particularities of each industrial or commercial sector. The collective intelligence needed to answer such challenges is well fitted by the ecosystem of thousands of SMEs and midcaps who can each develop tailormade solutions to answer specific issues relative to energy transition.

The genuine change is that these small and medium companies – once inexistent in the energy sector – are now a key component of the developments of new solutions for a low carbon economy. This is true on a stand-alone basis, but all the more as they enter into partnerships with utilities, public bodies and the investment sector that will enable robust investments and faster growth to the benefit of energy transition.

The second issue that arise is how to direct funds to these SMEs and midcaps. In this question lies probably one of the most critical bottlenecks that could impede the energy transition, as transitioning implies moving away from an established system to a new one. In trivial terms, we know for certain what we lose, and we hope to know what we gain4. There needs to be a demonstration of successful business models and business cases for the investments to pick up significantly. This means resetting the risk-return perspectives of the sector.

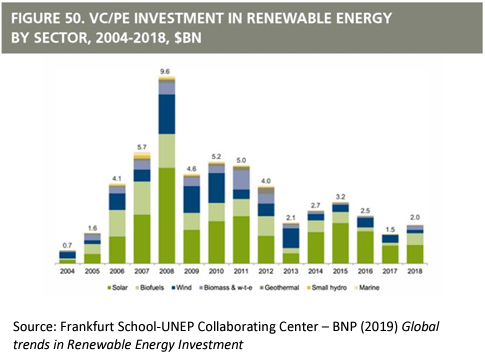

SMEs / midcaps in the energy sector are relatively new, 10 to 15 years in general. They constitute a nascent ecosystem, alongside the incumbent players. This relative novelty of these “energy entrepreneurs” means that the sector had to go through some inevitable infancy sicknesses: illdesigned subsidies schemes, poor asset performance, groping market designs, over-heated financing environment, etc. This has translated in a significant retreat of the PE and VC money from “clean techs” (see chart), which has often become a scarecrow word for investors.

In ten years, from the height of the late 2000s investment cycle to 2018, PE and VC investments in renewables have dropped by almost 80%. 2008 corresponded to the height of the “Renewables bubble”, driven by covlight financing, all-time high oil and gas prices and generous subsidies schemes, mainly in Europe. This first wave of renewables / clean tech development was driven by a political momentum, in particular by the implementation of the European Trading Scheme on CO2. It is interesting to note that what was a “niche” segment of the power sector at the time was from the beginning occupied by renewables entrepreneurs, incumbents being clear laggers (with the exception of Iberdrola).

After the financial crisis, the decrease in subsidies to renewables – and sometimes to changes in law during the subsidy scheme – led to IRR going from mid-teens in the late 2000s to mid-single digit towards the end of the 2010s. Furthermore, the disappearance of ultra-borrower-friendly financing let to bankruptcies and drastic reductions in the development pace of clean tech entrepreneurs.

We think that the cleantech sector must now be looked at with a fresh perspective. Since the early 2010s, a structural change has occurred in the sector with the cost of renewables plummeting, and digitization means that we gain much more intelligence on energy patterns than previously. It is on the backdrop of these fundamental changes that the survivors of the previous wave and a new wave of SMEs / midcaps have started to develop on a more robust basis: the cost of clean energy is often at par or lower than conventional energy and transparency and data have opened the way to new business models to increase the efficiency of the power system as a whole.

In fact, entrepreneurs are ideally placed to provide a large part of these solutions and develop new business models. But two questions must be solved for this to happen: 1) who will finance them, and 2) what is the risk-return profile that investors are ready to take to support energy transition.

Financing will of course come from various sources, from traditional bank loans to public support and classic equity rounds. But the issue is again the magnitude of the need. Directing savings towards the financing of the entrepreneurs appears to be a promising route. According to Eurostat, annual European households net savings amount to €940bn5. Roughly 70% of these savings are allocated to “assurance-vie” contracts and cash and deposits6. Whereas this pool of capital cannot be directed solely to investments in SMEs / midcaps nor to energy transition, the volume of money at stake can indeed make a difference.

While this amount of yearly savings is already significant and opens up opportunities, the key stake remains the stock of savings. In France alone, this stock amounts to €2,200bn for life insurance and cash and deposits. Reorienting this pool of capital was one of the motivations of the “Loi Pacte” passed in 2019 which allows to reallocate capital locked in French “assurance-vie” contracts (akin to long term- savings plan) to funds dedicated to the financing of SMEs / midcaps.

The problem – at least apparent – is that it would orient households’ savings towards investments considered as riskier: risk aversion is a reason why such a large portion of savings is channeled to bonds and deposits. As asset managers have a duty towards their clients to protect and value their investments, allocating more capital to SMEs / midcaps in the energy transition space requires a common will of both asset managers AND their clients.

In this perspective, distribution and investment strategies of large asset managers have so far been skewed towards infrastructure-like returns, providing attractive yield in a context of historically low interest rates. This trend led investors to invest massively over the last years in renewable assets on the backdrop of statebacked subsidies or power purchase agreements. Likewise, investments in networks, whose remuneration is determined by the regulator, provides the same kind of stable returns that fed the wave of investments in energy infrastructures over the last 10 years.

And yet, there is growing evidence that the appetite of retail investors for more sustainability / green investment opportunities is increasing7. In practical terms, this seems to suggest that retail investors are more aware of the impact of their savings and investment decisions and start to ask asset managers to invest in strategies that not only makes sense financially, but also from an ethical standpoint. Simultaneously, asset managers are increasingly committed in taking on systemic challenges such as the climate urgency. As their assets under management grow, several large institutional investors and asset managers recognize that their investment decisions send signals as to the sectors and companies that may be sustainable on all counts. In spirit, this is what the current trend on Green Finance is about: orienting more capital to sectors that make a difference on major issues such as climate change or biodiversity.

In our view, this is where one of the most critical transformation must take place in the investment sector if energy transition is to happen: the transformation of a complex system cannot be performed on the back of guaranteed returns. As entrepreneurs emerge and take risks to find solutions to the global issue of energy transition, investors will need to side and get comfortable with new risk-return patterns. This does not mean taking more risks, it means acknowledging that current investment decisions poorly reflect the reality of the underlying risks, in particular sustainability risks.

Our belief is that long-term perspective is critical to designing relevant investment strategies that provide both a relative security to investors and a capacity to support energy transition. Investing in SME / midcaps active in the energy transition can bear fruits in six to ten years, probably not in 3 years.

As renewables continue to decline in costs, as new technologies emerge along the whole power value chain, the industrial and market risks will take the center stage. Regulators and policy makers will in turn work to design regulations and a market architecture that will enable the management of these risks.

Entrepreneurs fit nicely into this emerging energy paradigm. Their DNA is to innovate and take risk, heeding clients or markets needs that they believe they can answer quickly, effectively, and minimizing the risk by focusing on their deep expertise of a particular aspect of the energy sector. They both thrive on and influence market designs and regulations.

To put it bluntly: energy transition will not be achieved through “secured” investments and will require endorsing new solutions and new business models to tackle this collective challenge. SMEs / midcaps, decentralized in nature, are well suited to take up focused challenges, enriching dramatically the collective intelligence of the energy sector as a whole. Investors will in turn need to apprehend the interest in accompanying companies whose value creation proposal lies in taking on the challenge of energy transition.

In an era of decentralization and deeper granularity, SMEs and midcaps should be the new players that funnel much needed capital if we are to achieve a fair energy transition. Eventually, the growth of SME / midcaps in this sector will go hand in hand with the development of sustainable finance. At the core of sustainable finance lies the idea of investing long-term and to price-in social and environmental externalities. Investing in the growth of SMEs / midcap active in the energy transition space is a powerful way to do so.

1 Although on this particular topic, one could argue that the social and environmental consequences of climate change should precisely be the reason for states to invest in energy transition. Investments in this sector are characterized by massive externalities, which are much better accounted for in public investment policies than in private investments. The purpose of public policies being – at least in spirit – the maximization of general good, states are central to orienting society and economy towards sustainability, just as the Paris Agreement shows.

2 The use of any CO2 pricing proceeds for example would play here a major role: redirecting those proceeds to smoothen the cost of energy transition, especially for Europeans in situation of energy poverty or at risk thereof, is a promising path. This topic has been discussed in a contribution of TiLT Capital to the debates of the Task Force on Carbon Pricing in Europe.

3 These figures do not include the midcaps (reliable data are not easily available).

4 See the point made by the Energy Transitions Commissions on this particular topic: http://www.energytransitions.org/sites/default/files/ETC_Insights_Scaling-Investment.pdf

5 https://appsso.eurostat.ec.europa.eu/nui/submitViewTableAction.do

7 See the 2019 Kantar Survey for BNPP AM (https://docfinder.bnpparibas-am.com/api/files/674AE21E-F334-4F7C-9738298CA1CDF0BF) or the 2018 Deloitte European SRI Study for Eurosif (https://www2.deloitte.com/content/dam/Deloitte/lu/Documents/sustainable-dev/lu-european-sri-study-2018.pdf)