Almost three years ago, we issued TiLT Perspectives #5 titled “Dethroning King Coal”. The message was simple: we must take coal out of the energy equation if we are to succeed on our fight against climate change. To do so, we argued that renewables and gas (and nuclear to a lesser extent, due to long construction time) were the right mix of the next 15 years.

Simple, and quite provocative according to some of the reactions we had: we were proposing to “lock in gas emissions”, to “give the O&G industries reasons not to change”, etc. That was in 2020. Since then, Russia has invaded Ukraine, gas prices have gone through the roof, and security of supply has become one of the hottest hashtags in media. To energy players, it has always been a concern, and I dare to say it has always been a hard nut to crack.

So, in a time when “gas” seems to be a cursed word, let’s talk about gas. And in fact, let’s talk about why we still believe that gas needs to be part of the energy equation of the next 15-20 years, and under what conditions. One central issue here will be fugitive methane emissions. We will also try to lay out some of the solutions that we see as key to tackle that issue and that call for significant investments and R&D.

Methane is so much worse for climate change than CO2… in the short run.

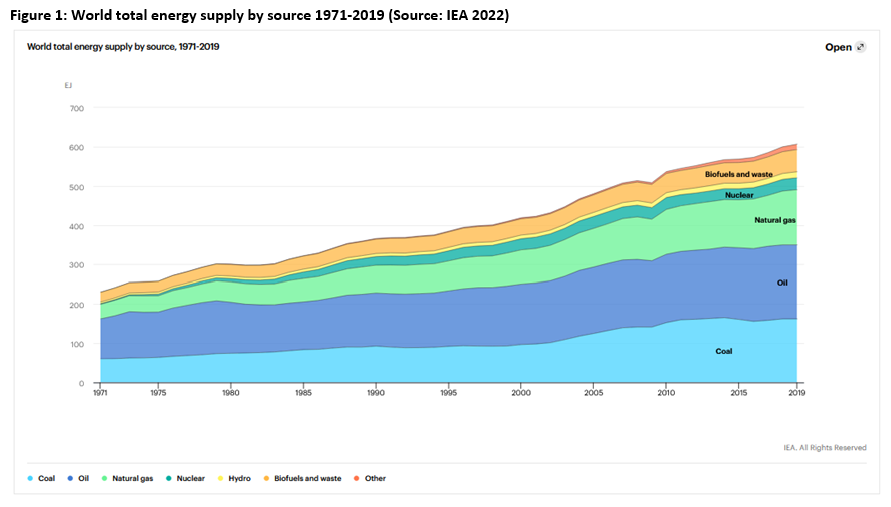

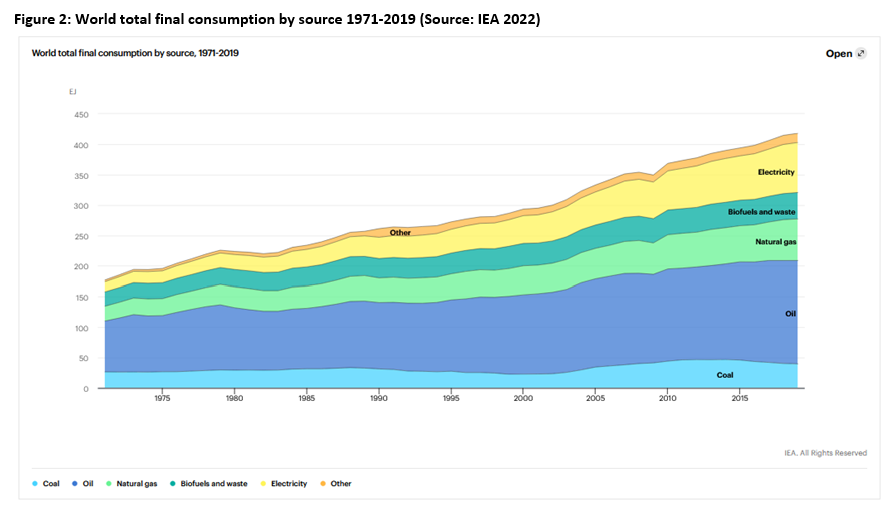

Let’s start off with the obvious: in 2020, fossil fuels accounted for 80% of energy sources worldwide (Figure 1) and roughly 60% of final energy consumption (Figure 2). The reasons are multiple, but rely mostly around ease of use, storage and transportation and energy density. To be clear, over the last 50 years, the share of fossil fuels decreased, mainly due to the development of nuclear and to a lesser extent of renewable energies. But in absolute terms, fossil fuels consumption doubled.

As mentioned in our previous piece, the implication is that the level of investment in RES capacity and storage would be huge to replace dispatchable and energy-dense fossil fuels. Hence our view that gas should be a transitory fuel alongside renewables. Simply put: we do not see a path whereby RES, batteries and H2 alone enable a drastic reduction in fossil fuel consumption in the next two decades, we need to pick our battles. In electricity generation, the benefit appears clear with gas having an emission factor 40% to 50% lower than the different types of coals.

Global warming potential and Short-Lived Climate Forcers

This situation established, it is critical to take into account externalities and the whole value chain of each energy source to assess its merits and drawbacks.

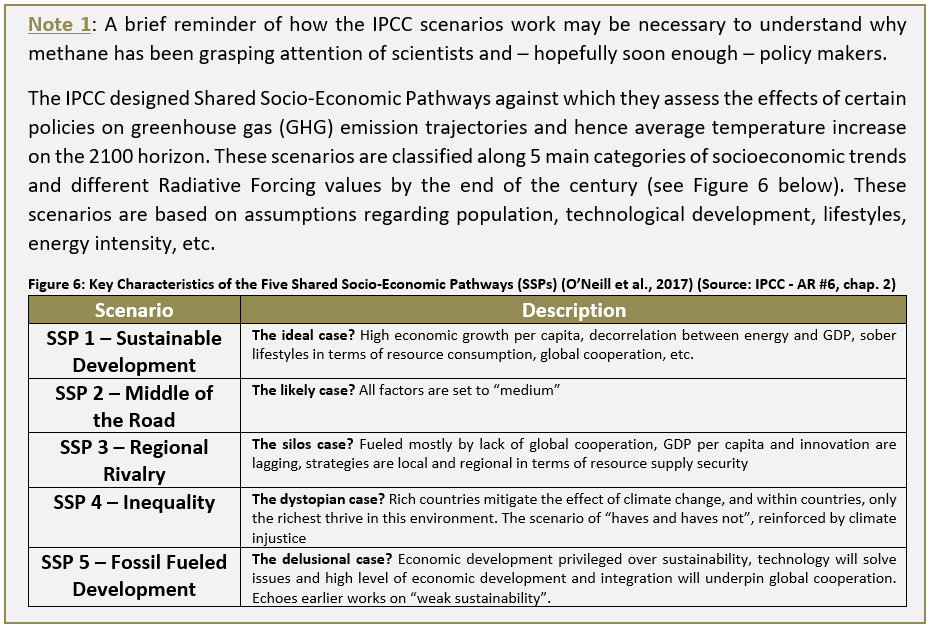

The 6th Assessment Report of the IPCC (Intergovernmental Panel on Climate Change), which has been released in August 2021 while the synthesis is expected by March 2023, puts a particular emphasis on Short-Lived Climate Forcers (SLCF) in general and methane in particular, due to their potent Global Warming Potential (GWP). The 6th Assessment Report of the IPCC defines SLCF as “a set of chemically and physically reactive compounds with atmospheric lifetimes typically shorter than two decades but differing in terms of physiochemical properties and environmental effects.”

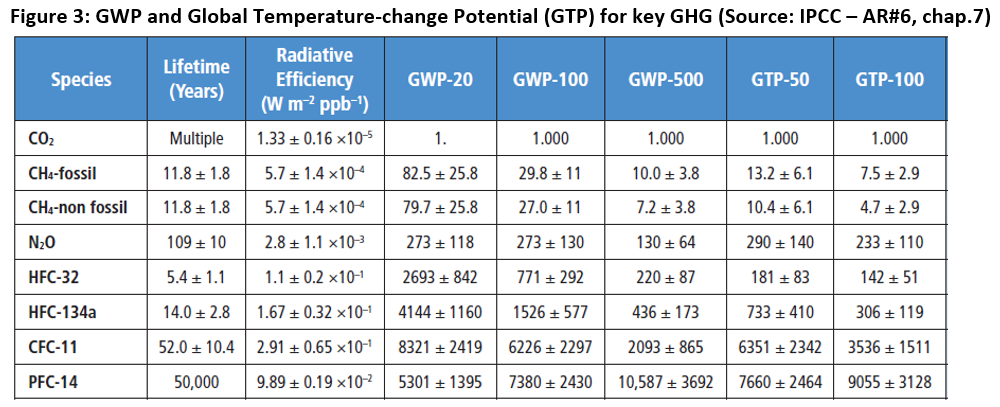

GWP is a measure of the extent to which a gas traps heat in the atmosphere. There are two elements to understand GWP: 1) the unit, which is a ton of CO2 and 2) the period of time over which this greenhouse impact is measured. The most common measure is GWP100, meaning the GWP over 100 years.

CO2 has a lifetime in the atmosphere varying from 300 to 1000 years, and its GWP is by definition equal to 1 over this period of time. By comparison, Nitrous Oxide (N2O) remains intact during an average 109 years in the atmosphere, before it gets absorbed by a sink or deteriorated by hydroxyl radicals contained in the atmosphere. Its GWP is however much greater than CO2 during this period of time: 273 tCO2eq over 100 years but 130 tCO2eq over 500 years (see Figure 3).

We see here why methane matters: despite a lifetime of only 12 years, it has nevertheless a short-term impact 83 times higher than that of CO2, hence its belonging to the Short-Lived Climate Forcers group. These characteristics have a profound implication on climate policies: whereas CO2 represents a “stock” issue – i.e. it accumulates in the atmosphere over a long period of time, leading to global warming, CH4 represents rather a “flux” issue – it has a massive impact in the short term, but does not accumulate over the long term in the atmosphere.

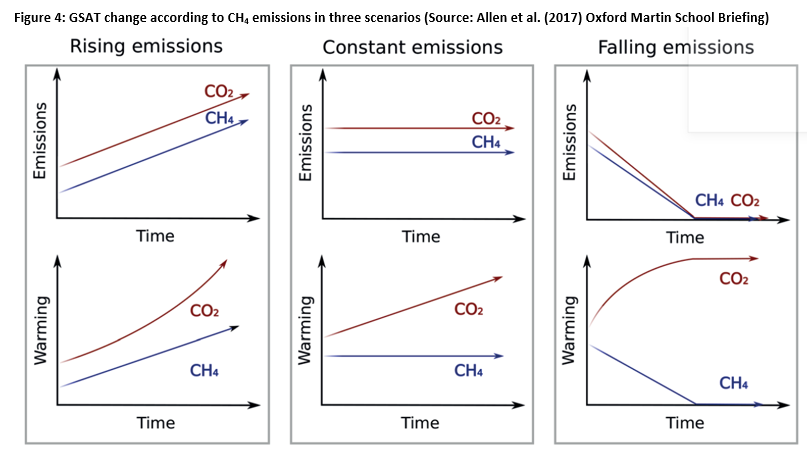

This is well illustrated by Allen et al. (Figure 4): in a scenario of constant emissions (central scenario), a constant flux of CO2 emissions over time leads to a build up of CO2 stock in the atmosphere, because CO2 is decaying over a very long period of time, leading eventually to constant increase of temperature due to greenhouse effect. On the other hand, methane decaying in 12 years on average, a constant rate of emissions does not increase temperature.

IPCC scenarios and new measurement of GWP taking into account SLCF

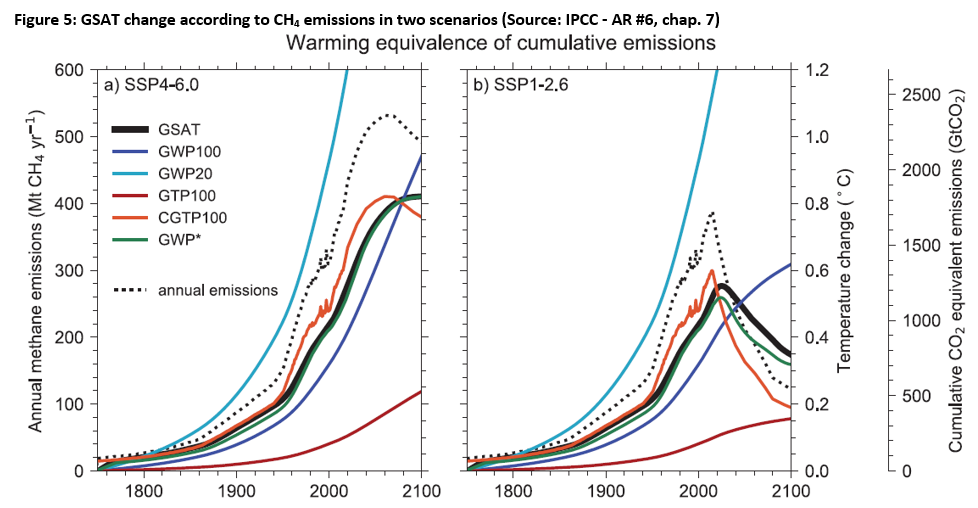

Hence the call by the IPCC to drastically curb methane emissions, as it would quickly and greatly contribute to putting the world on a Paris Agreement trajectory. In its chapter 7 of the AR #6, the IPCC shows the impact of CH4 emission reduction on Global Surface Air Temperature (GSAT – a measure of global warming). As displayed in Figure 5, models tend to show a strong correlation between GSAT and annual methane emissions (dotted line and bold black line), here in two IPCC scenarios: SSP4-6.0 and SSP1-2.6.

Methane emissions: what are we talking about?

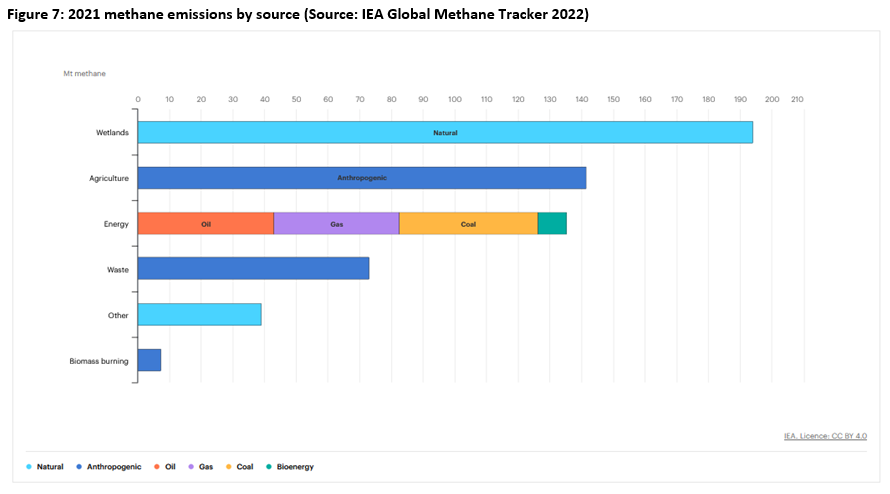

The issue is hence direct emissions of methane into the atmosphere, be they from natural origin or due to human activities. Figure 6 shows the volumes of methane emissions as estimated by the IEA. “Estimated” must be emphasized, as one of the main tasks today is to adequately measure and quantify these emissions, whatever the origin.

According to the IEA, nearly 590 Mt of methane have been emitted in 2021. Natural sources (wetlands in particular) account for 40% of these emissions, while anthropogenic emissions account for 60%. This estimate is coherent with the first Global Methane Assessment report of the UNEP and the Climate and Clean Air Coalition, which evaluates global methane emissions in 2017 at 590 Mt in its “top-down” approach, based on atmospheric observations. However, in the same report, a “bottom-up” approach based on activity data by sector multiplied by an emission factor leads to a figure of 750 Mt of methane emissions.

Whatever the methodology and the source, anthropogenic emissions account for the largest share of emissions. Using the GWP mentioned above, the impact of man-made methane emissions is staggering: if we consider an emission figure of 360 Mt at a GWP20 of 83, the short-term impact of methane emissions is equivalent to releasing nearly 30 GtCO2eq into the atmosphere every year, or over 50% of all GHG emissions. Obviously, focusing on a GWP100, the impact of methane is much lower: those same 360 Mt is equivalent to roughly 11 GtCO2eq, or 20% of the global emissions.

This figure alone explains the emphasis put by the last IPCC report on SLCF and methane.

When zooming in on the sectors, several takeaways come to mind, other than the obvious results regarding the share of agriculture (cattle) in these emissions and that of the energy sector:

- Fugitive methane emissions (unintended emissions resulting from human activities) are split roughly equally between oil, gas and coal. The first implication is that the argument against replacing coal with gas because of fugitive emissions does not hold: taking out coal means taking out the largest single source of CO2 emissions by far, and taking out a significant methane emitter, due to coal bed methane fugitive emissions. Indeed, based on these figures, an increase in gas use in the power mix would also translate into higher fugitive emissions, which must be avoided;

- Waste is an often-overlooked emission source. It represents today 20% of anthropogenic emissions of methane. The worrying trend comes from the increase of waste, against the backdrop of consumerism and population growth. The World Bank estimates that the 2bn tons of solid municipal waste generated each year could become 3.4bn tons in 2050. 70% of this waste is disposed of in landfills and open dumps, while only 8% of global landfills are equipped with gas collection systems.

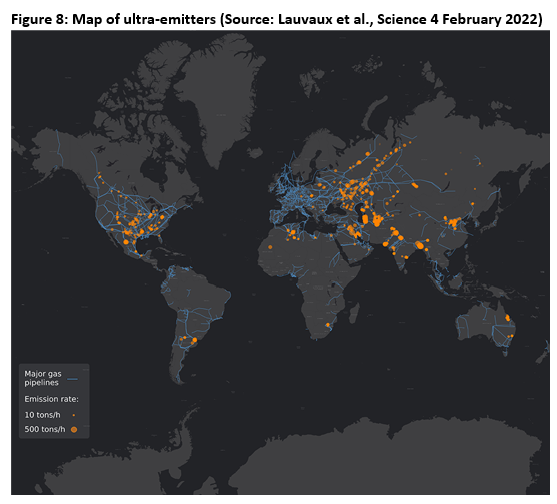

When focusing on the energy sector, the oil and gas sector draws specific attention due to the magnitude of fugitive emissions, but also to the impact of uncontrolled leaks. A study by Lauvaux et al. from the Centre National de la Recherche Scientifique (Science, Feb. 2022) focused on so-called “ultra-emitters”, i.e. operations with a methane emission rate over 25t/h. Using satellite imaging, this team came up with 1,800 ultra-emitters in the world, of which 1,200 attributable to oil and gas operations and accounting for at least 12% of O&G CH4 emissions.

Figure 8 shows the location of these emitters, and unsurprisingly, they mirror the map of the major oil and gas operations, but not only exploration and production (US, Middle-East, Russia), but also transportation and distribution. It is obvious when looking at the greater European region including Russia: many of these ultra-emitters concentrate on the routes of the major gas pipelines bringing gas from Russia to Europe. It also shows the major Asian cities in China and India for example, where leaks occur on the gas distribution networks.

The challenge for the oil and gas industry in the short run is hence the management of these leaks and especially of the ultra-emitters. The massive gas leak of the storage facility outside of Los Angeles in 2015 released 100,000 tons of methane, or the equivalent of 8Mt of CO2 in just four months due to equipment failure. Not so long ago, in December 2021, the European Space Agency captured the release by a platform in the Gulf of Mexico of 40,000t of CH4 in just 17 days.

Much more than the use of methane for electricity production (which translates into CO2 emissions, but in much lesser proportions than coal) or for industrial applications (including hydrogen production through Steam Methane Reforming, also translating into CO2 emissions in the end), the issue of methane is the key point that needs to be tackled in the industry and at the heart of investment strategies to curb and ideally suppress these fugitive emissions.

Implications for industrial and investment strategies

This painting of the methane emissions situation shows how critical it is to curb methane emissions to put our world on the Paris Agreement trajectory. According to the UNEP, a 45% reduction in anthropogenic methane emissions would suffice to put us on the right path.

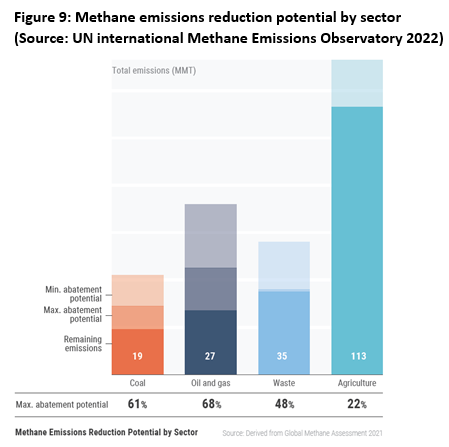

The good news is that a number of solutions already exist and are fairly easy to implement. The bad news is that they have not been put in place yet mostly out of lack of political will or economic incentives. The 2021 Global Methane Assessment report estimates the reduction potential for the key sectors of agriculture, energy and waste (see Figure 9).

Coal: abatement potential of ~23 Mt, of which 13 Mt accessible in the short term. It implies pre-mining degasification and recovery, oxidation and ventilation of air methane, flooding of abandoned coal mines (which unfortunately require massive volumes of water).

Oil and gas: abatement potential of ~35 Mt, of which 20 Mt accessible in the short term. As the studies on ultra-emitters suggest, this is mostly a matter of operational efficiency and quality of operations. It entails regular inspections (and repair) of sites, replacing pressurized gas pumps and controllers with electric or air systems and replacing outdated equipment with more efficient versions, in particular electric versions vs. pneumatic or gas or diesel-powered engines. It also calls for capping systematically unused wells.

Waste: abatement potential of ~20 Mt requiring recycling, re-using, no landfills of organic waste, landfill gas recuperation and valorization, improved anaerobic treatment of wastewater with biogas recuperation, etc.

Agriculture: the abatement potential is only ~25 Mt out of 140 Mt, unless we move decisively away from meat-rich diets globally.

We derive two policy and investment implications from this analysis.

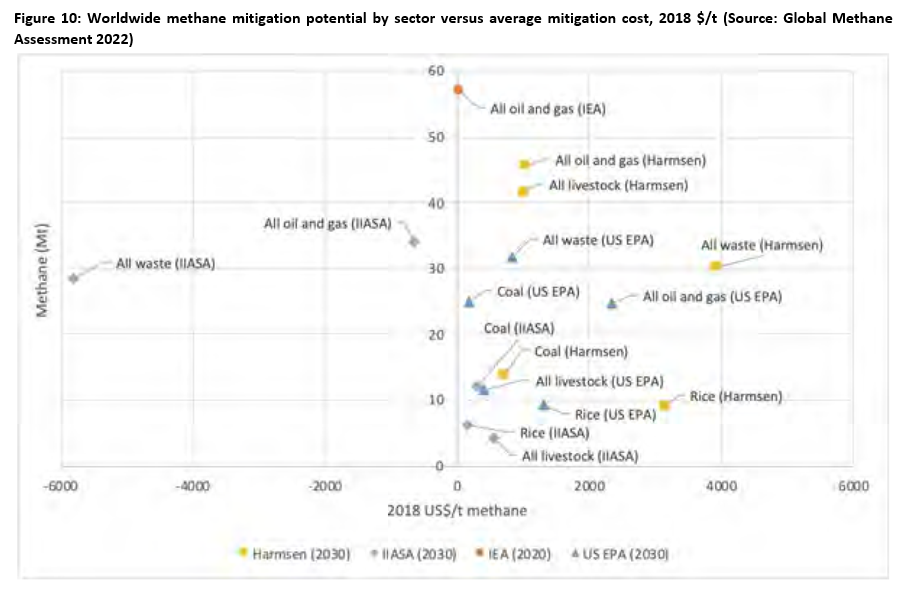

- The current economic tradeoff made by the oil and gas sector is that it is better to allow for these fugitive emissions to happen rather than investing in the necessary technologies and solutions to prevent them. However, pricing the externality attached to fugitive methane emissions appears absolutely necessary to drive the oil and gas sector to invest more thoughtfully in curbing fugitive emissions1. On the cost of this abatement, studies vary greatly between the IEA, the US EPA, IIASA, etc. but according to the IEA and the US EPA, at least 60% of the emission reduction could be achieved with a price of 600$/t of CH4 (or 7.3$/t in CO2eq considering GWP20 of 82), considered as “low-cost measures”.

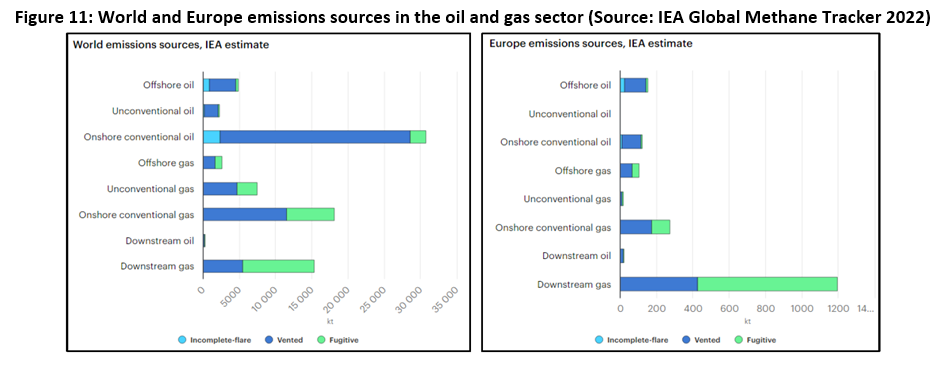

- The second policy implication is probably more specific to Europe: the Taxonomy formally excludes from “green investments” any oil and gas sector related investments. The immediate implication is that funds, banks etc. are more and more reluctant to invest in companies that provide solutions for the oil and gas industry. Whereas it appears legitimate for the EU policy makers to avoid locking in investment incentives for this sector, a sound climate policy should point to improving the operational efficiency of the oil and gas sector.As mentioned in the first part of this paper, it appears delusional to think that we will avoid relying on fossil fuels in the next 10 to 20 years. Therefore, investing in solutions that will drive a massive reduction in CO2 AND methane emissions at low costs is probably one of the most effective strategies. In particular, Europe could focus on the downstream part of its gas system, that accounts for the bulk of its methane emissions according to the IEA (see Figure 11).

With the depletion of historical basins in the UK, the Netherlands, and Germany, and the creaming curve flattening in Norway, Europe is not anymore a hotspot of oil and gas operations. However, Europe has a large industrial ecosystem in relation to oil and gas, with deep levels of expertise, be it in services, infrastructure, exploration and production or refining. Relying on this expertise to design cost-efficient solutions towards more sustainable industrial processes in the short term could be a winning strategy both for the EU climate ambitions, the big names and smaller players of the sector and could help mitigate the cost impact of the energy transition.

Critical choices at the heart of sustainability

Against the backdrop of the war in Ukraine and its impacts on global energy markets, the risk is that security of supply – especially in Europe – prevails over the urgent need to curb GHG emissions and opposing sides often take strong stances in this debate; on the one hand, so-called “realists” garnered momentum and are increasingly vocal in saying that we cannot breed growth without oil and gas, on the other hand so-called “climate defenders” are adamant that fossil fuels should be banned all together.

Unsurprisingly, we will take an approach linked to what seems both ambitious and feasible, based on a forgotten concept of the 1987 Brundtland report: “critical choices”. If a straightforward solution existed to fight climate change while preserving short-term economic growth and current lifestyles, it would have emerged. The reality is probably very different: a much needed new paradigm can only be implemented through a succession of tough decisions (“critical choices”), each imperfect on many counts, but each putting us on the right trajectory.

The good news is that thanks to the works of the IPCC and scientists over the world, we may have very powerful short-term choices to make that are less “critical” than many others: by investing in and implementing solutions that curb drastically anthropogenic methane emissions, we could walk much of the road to the target of the Paris Agreement.

The only critical choice to be made is to avoid simplistic views – even well-intentioned ones, and work actively towards this “demethanization” of key sectors such as energy and waste. It will give greater value (both environmental, economic and social) to the shift from coal to gas, combining the effect of removing a massive flux of GHG emissions (methane) with that of avoiding building a stock of long-lived GHG emissions (CO2).

[1] The Task Force on Carbon Pricing led by Edmond Alphandéry (former French minister of economy and finance and former Chairman of EDF) initiated works on this matter, with a round table on this topic held in December 2022 as part of the Policy Dialogue II organized by the International Finance Forum of China.