Nicolas PIAU

Founding Partner & CEO

Member of the Siparex Executive Committee

PERSPECTIVES #11

The use of fossil fuels and their associated GHG emissions will decrease as we transit to a low-carbon economy, yet extractive industries remain at the heart of both environmental and digital transitions.

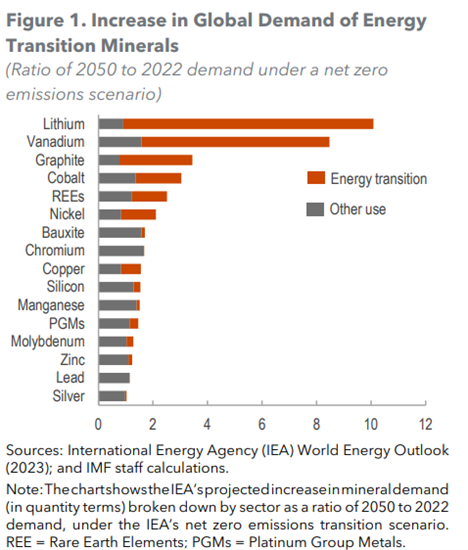

Figure 1 – Increase in Global Demand of Energy Transition Minerals (Source: IMF 2024 [3])

Altogether they are referred to as critical raw materials (CRM), due to the economic role they already play today which will keep increasing in the foreseeable future as demand is expected to be multiplied by more than 2 by 2030 according to the IEA (in the Announced as Pledges Scenario) and 3.5 by 2050 (in the Net Zero Emissions Scenario).

Even copper demand, at 26 million tons in 2023, is set to increase roughly twofold over the next 25 years, driven by the trend towards electrification 4.

To meet the expected demand for critical minerals, both recycling and diversification of sourcing will be core components of geopolitical strategies, however we chose to focus on the extraction side of the issue. Securing the supply of these minerals is crucial but comes with a number of challenges to tackle.

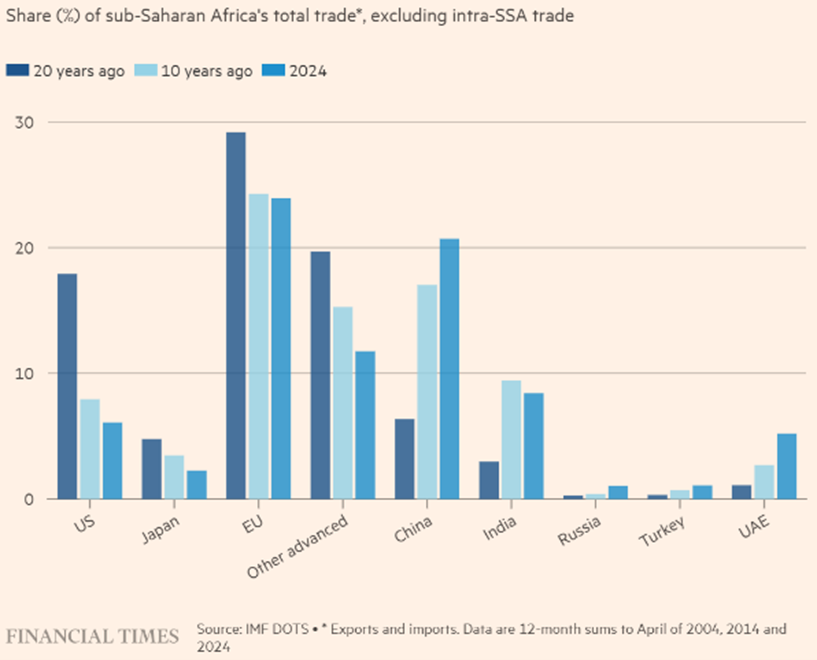

Figure 2 – Sub-Saharan Africa’s total trade (Source: FT 23 Aug 2024 [8])

China’s long-term vision to build its dominance on global supply chains

A major player in the critical minerals supply chain

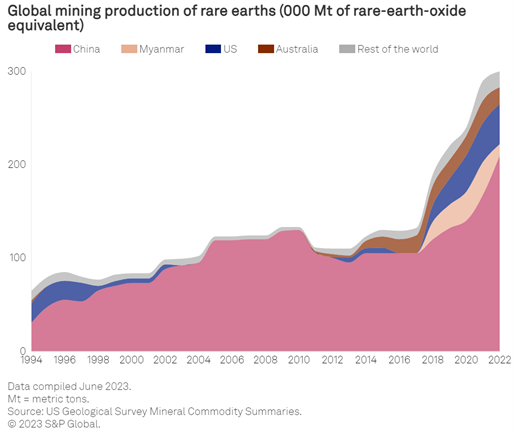

Figure 3 – Global mining production of rare earths (Source: S&P 24 Aug 2023 [10])

China has a long history in the production of critical minerals which started in the 1950s with REE. REE were declared protected and strategic as early as 1990, thus restricting the involvement of foreign investors in rare-earth mining in China. Over the 1990s and 2000s, the share of Chinese output in the total REE production increased to reach 129,000 tons in 2009 up from 16,000 tons in 1990 while the rest of the world’s fell from 44,000 tons to 3,000 tons over the same period9, mostly driven by the low production cost and a loose environmental regulation in China.

In parallel, China’s consumption of REE started to increase after 2000 with the development of midstream and downstream activities, leading Beijing to invest massively in the supply chain serving local demand and to progressively build a quasi-monopoly on REE supply chain with 60% of mining and 91% of refining global capacity11.

The same vertical integration strategy goes for battery components: the rapid growth of the demand for EVs in China and the volatility of raw material prices, especially for lithium, have led to a vertical integration of Chinese battery-manufacturers over the past few years up to the point where 2/3 of global lithium supply are processed in China whereas the country only accounts for 13% of global extraction of lithium12.

To ensure the availability of raw materials to its midstream and downstream industries, China started to secure overseas supply in particular via the Belt and Road Initiative (BRI) launched in 2013 which pursues multiple and complementary objectives: (i) find new markets for Chinese industries, (ii) secure their supply chains and (iii) serve as an influential tool promoting a new global economic order.

Massive investments in overseas extraction activities

China has been an active investor in Africa, financing major infrastructure projects in mineral-rich African countries early in the 2000s such as Zambia (copper), the Democratic Republic of Congo (DRC) (copper, cobalt), South Africa (iron ore) as well as Zimbabwe (platinum)13.

This trend has been further accelerated by over $1,000bn14 of investments pledged under the BRI framework and Beijing has entered into 200 cooperation agreements with 150 countries in particular in Asia, Africa and Latin America. Through construction contracts financed with loans provided by Chinese financial institutions and investments in equity, China has progressively reinforced its presence in Africa, in particular in the above-mentioned countries and Guinea15.

Even though investments in the continent are significant – in 2023, Chinese investments in metals and mining reached $19.4bn16 representing 21% of the country’s overseas budget17, with Africa as the largest recipient – only 8%18 of the African mining sector is controlled by China (while Western companies control twice this amount). Yet, this low percentage hides a variety of situations. As an example, Chinese companies own 72% of DRC’s cobalt and copper mines and have increased their investments in lithium mining in Zimbabwe – all of these materials being essential to the manufacturing of batteries. China has also become the largest buyer for the African mining sector: in 2019, nearly $10bn worth of minerals were shipped to China to be processed 19.

Chinese dominance in a context of rising geopolitical tensions

This long-term vision supported China’s dominance on the critical minerals market, and made it become the global lead producer of 22 metals and 7 industrial minerals20.

This dominance creates dependence and vulnerability for all other countries and their industries. Until the end of the 2000s, little attention was paid to such concentration of the supply chains but in 2010, China set stringent quotas on exports of REEs to prioritize its domestic demand. A couple of months later, Japan experienced disruptions of imports and accused China of putting an embargo in the context of a dispute in the East China Sea. Following these events, countries relying on imports from China started to worry about the concentration of their supply chains and started to work on supply diversification by (i) finding alternatives to China, (ii) making use of Chinese black market for rare earths, (iii) developing recycling solutions, and (iv) developing new mines outside of China, however with limited effects.

The crisis in the early 2010s shed light on the concentration of extraction activities, but it did little to prevent China to keep building its supremacy in the processing phase and to become a massive importer of critical minerals.

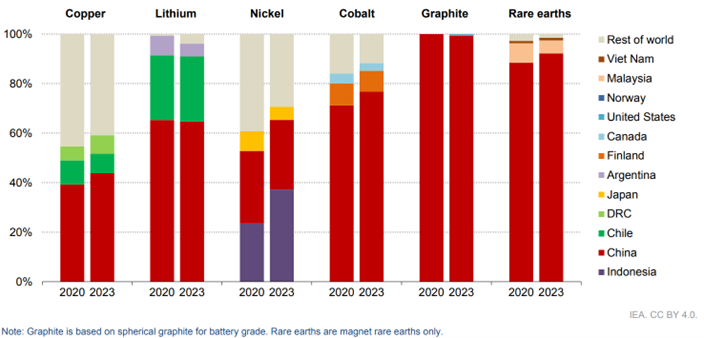

Figure 4 – Share of refined material production by country (Source: IEA 2024[21])

Mid-2023 China announced export controls on gallium and germanium, followed by graphite and a ban on rare earths processing technologies and permanent magnet production technology from December. In August 2024, Beijing further tightened its policy, announcing export controls on antimony, used as flame retardant, photovoltaic glass, lead acid batteries, as well as in the defense industry. The initial measure was taken as a response to Washington’s export controls on semiconductors as well as on the equipment and expertise to produce them. By weaponizing critical minerals, China aims to leverage its dominance of the supply chains, but this strategy has its limits as it could also ultimately weaken the country’s position by (i) further incentivizing Western countries to develop alternative sources of raw materials (see on Figure 3, the diversification of REE production following Chinese export controls of the end of the 2000s) and (ii) by exposing itself to further restrictions while Beijing is crucially dependent on some downstream technologies.

In today’s situation, many industries heavily rely on Chinese supply chains while the use of the REE and other critical minerals only increases with the energy and digital transitions. This has led many countries to implement policies to reduce their dependency to China: the EU CRMA, US IRA, Australia’s Critical Minerals Strategy, Canada’s Critical Minerals Strategy, etc.

The EU’s ambitious response to such dangerous disbalance: the CRM Act

EU’s high dependency to overseas minerals

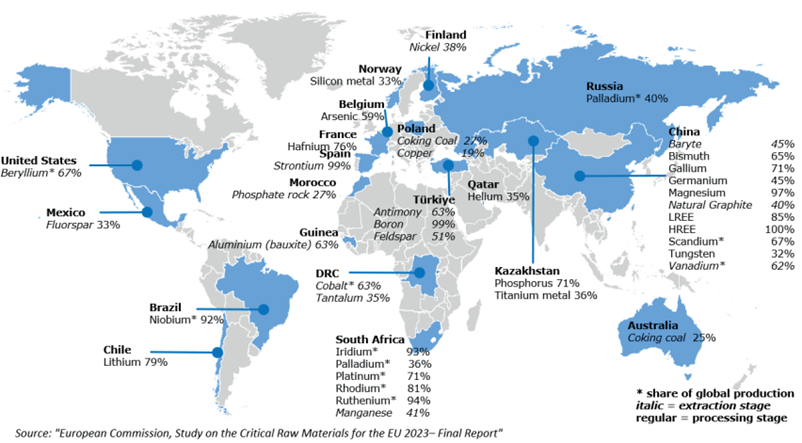

The EU has been measuring its dependency on CRM for more than a decade with a first report released in 2010. The latest version of this assessment shows very high dependency to a single country for some of elements: 99% of the boron consumed by the EU is extracted in Turkey, 92% of the niobium comes from Brazil, and a lot of elements (extracted or processed) comes from China such as REE (100% for the High REE and 85% for the Light REE) or magnesium (97%).

Figure 5 – Major EU suppliers of CRMs (Source: European Commission 2023)

Despite this early awareness and the implementation of the Raw Material Initiative (2008), the situation has not significantly improved.

Enhancing EU’s independency with the Critical Raw Materials Act

With the EU setting ambitious objectives of decarbonization (the Green Deal), the need for a regulation to promote resilient critical raw materials supply chain had become crucial. The Critical Raw Materials Act (CRMA) was announced in 2023 with the Green Deal Industrial Plan and adopted in 2024 in a record time.

The CRMA identifies Strategic Raw Materials (SRM) whose importance exceeds that of the Critical Raw Materials (CRM) due to their use in strategic sectors (energy transition, digital, defense, etc) and sets (non-binding) objectives by 2030 for them:

The CRMA creates a favorable framework (i) to promote the exploration and extraction activities within the EU and (ii) to conclude partnerships with third countries. It however relies on existing financing instruments only and does not create a long-term financing instrument or commitment.

On the domestic side, the CRMA aims at simplifying the permitting process and facilitating access to finance, in particular for strategic projects which benefit from an accelerated procedure and the elaboration of national exploration programs. The objective is to create favorable conditions for the development of and the investment in mining projects.

However, the high cost of energy compared with other geographies (such as the US), especially during the energy crisis in the aftermath of Russian invasion of Ukraine, can prevent the installation of processing industries in Europe despite Europe being the continent with the electricity mix showing the lowest carbon intensity.

Overseas, the EU implements its strategy relying on two main financing instruments.

The Global Gateway Program has been implemented since 2021 with a budget of €300bn for the period 2021-2027 in order to “boost smart, clean and secure links in digital, energy and transport sectors and to strengthen health, education and research systems across the world”; it is designed as an alternative to the Chinese BRI. Within this framework, the EU has signed Memorandums of Understanding (MoU) with several African countries such as the DRC, Zambia and Rwanda, but implementation of these agreements remains to be seen.

The European Investment Bank (EIB) as the world’s largest international public bank with a total balance sheet of around €600bn has a key role in building resilient supply chains. The bank must support EU’s strategic priorities, hence the inclusion of the financing of projects in line with the EU’s Global Gateway in its 2024-2027 roadmap. The EIB also signed a strategic partnership with Rwanda on CRM investments22 with the objective of unlocking new opportunities and developing new jobs in the country.

Despite these initiatives, no investment directly related to CRM projects has been made so far under the Global Gateway framework, while the EIB has not yet engaged in financing mining or refining projects. While its ESG standards pave the way for the emergence of sustainable mining, the EIB must necessarily rethink the best way to support such projects to accelerate decision and stand out as a reliable partner to African countries.

Being able to finance projects abroad being a prerequisite to secure resilient supply chains, some Member States decided to take action at a national level and developed their own funding instruments. For instance, France, Italy and Germany have launched their metals investment funds23.

In parallel, the EU is engaged in various partnerships or multilateral projects.

The Lobito Corridor: the EU contributes to the Partnership for Global Infrastructure and Investment (PGII), an initiative launched by the G7 to fund infrastructure projects in developing countries with a $600bn budget. Under the PGII, multi-stakeholder agreements have been finalized with the DRC, Zambia and Rwanda to develop the Lobito corridor, a rail line that will connect the port of Lobito in Angola with the copper belt in Zambia and the DRC24 and which is supposed to bring sustainable growth to the region. However, critics of the project point out that it focuses on exporting raw materials through a direct route with limited benefit for the region, thereby repeating the schemes that have not allowed the continent to develop midstream capabilities and to leverage its natural resources to fuel its development.25

The Minerals Security Partnership (MSP) is an initiative to create more responsible and resilient critical minerals supply chains which is composed of 14 (mainly Western) countries and the EU, which launched the MSP Forum in April 2024. This forum, co-led by the US and the EU, gathers the 15 partners of the MSP, mainly countries with a high demand for CRM, and 15 resource-rich countries (Argentina, Ecuador, the DRC, the Dominican Republic, Greenland, Kazakhstan, Mexico, Namibia, Peru, the Philippines, Serbia, Türkiye, Ukraine, Uzbekistan and Zambia) to work on the development of sustainable, diversified and resilient supply chains.

The African continent at the heart of a global competition

Securing access to critical minerals has become a strategic concern across the world, and Africa, being home to 30% of global reserves, finds itself in the middle of a global competition.

The US: a necessary renewed strategy in Africa

Historically, the US had been a major producer of minerals before increasingly shifting to imports. As of today, 31 of the 35 CRM defined by the US Department of the Interior are imported (in total or to complement local production) and half of them are refined in China26. Conscious of this vulnerability, especially in a context of commercial tensions with China, the following priorities have been identified to boost domestic production: (i) opening of new mines with accelerated permitting processes, (ii) reprocessing of mine wastes, and (iii) recovering byproducts from operating mines. In parallel, the US must develop its processing and manufacturing industry to avoid exporting critical minerals in a raw state and importing value-added products27.

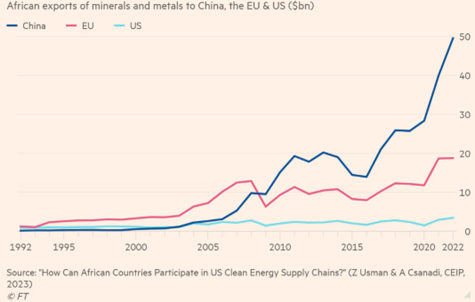

Figure 6 – African exports of minerals and metals to China, the EU and US (Source: FT 8 Feb 2024[29])

On the external side, the US primarily focuses on cooperation with allies such as through the PGII, the MSP or with countries with which it shares common interests such as the Gulf States. Indeed, the US has not historically maintained strong ties with African countries and the continent accounts for less than 2% of US global commerce28, despite the trade programme in place (the African Growth and Opportunity Act).

The US needs to rethink its policy vis-a-vis Africa. Biden’s administration gave a huge push to deepen the relations with Africa by committing at least $55bn to the continent over the next three years at the US-Africa leaders’ summit in December 2022, including private sectors initiatives of more than $15bn 30. Regarding the production and refining of critical minerals, the US International Development Finance Corporation is supporting 7 projects for a total of $412m in South Africa, Mozambique, Rwanda, Tanzania, Guinea and Brazil31.

The country has signed several MoUs with countries located in South America, Asia and Africa (Tanzania, DRC, Zambia), however there is not always a clear follow-up to these agreements. In parallel, the US has passed several acts such as the Inflation Reduction Act (IRA), the CHIPS and Science Act, the Infrastructure Investment and Jobs Act, etc. However, the IRA does not apply to minerals sourced from Africa due to the absence of Free Trade Agreements with the region, which can partly undermine the bridging efforts vis-a-vis the continent 32.

The recent elections will have an impact on US critical minerals strategy: both Republicans and Democrats consider this issue as a major challenge, however their answers and priorities differ. Under a Trump presidency, we can expect increased efforts put on domestic extraction and processing projects where Biden administration prioritized a friendshoring strategy. Accordingly, the US is likely to show a lower level of involvement in international collaborative initiatives, thereby potentially degrading relationships with allies such as Europe33.

Middle East’s entry into the race

For Middle East countries whose wealth has been built on oil and gas, the energy transition may be a driving force to reshape their industries. Saudi Arabia’s strategy to diversify its economy was presented in its “Vision 2030” 34 which highlights the importance of mining as the country owns $2.5tn of mineral resources in its soil35. In parallel, the region needs to secure the supply of critical minerals as it is also engaging in the energy transition and, as aforementioned, such materials are crucial for its industries.

Historically Saudi Arabia and the United Arab Emirates (UAE) were tied to the US, however the post-oil era has ushered in a restructuring of relationships and partnerships. Even though the US remains an important partner, the countries have also developed ties with China and the global South, because future growth will come from large and dynamic markets such as India, South America and some African countries. This strategy finally serves the objective of both countries to become new poles in a multipolar world.

Gulf countries can offer advantages beyond their financial resources to African countries: their experience in a related sector – oil and gas exploitation – can prove to be helpful to develop the value chain around the exploitation of other natural resources (energy and logistics management), plus their success in leveraging their natural resources to fuel their economic development.

Saudi Arabia, from oil to metals?

Riyadh’s strategy displays three components: (i) developing mining activities in Saudi Arabia due to its vast and resource-rich territory, (ii) securing supply from overseas, essential to develop other industries and (iii) becoming a major actor between Africa and Asia thanks to its geographical location and its strengths.

Investments abroad: To achieve this objective, Manara Minerals, a joint venture between state-owned mining company Ma’aden and Saudi Arabia’s Public Investment Fund, was established in 2023 to invest in mining assets globally and a first investment in Brazilian Vale Base Metals Limited for a 10% stake was disclosed. The company and the country have reportedly been active in several critical minerals deals: it has expressed interest in investing in Democratic Republic of Congo36, and is said to be a potential bidder for up to a 30% stake in Zambian copper mines owned by Canadian First Quantum Minerals, alongside Rio Tinto, Chinese and Japanese companies37. On top of that, the Saudi Fund for Development signed agreements amounting to $533m with African countries38.

Figure 7 – “Super Region” (Source: Wood Mackenzie 17 Jan 2024 [40])

Super Region: Riyadh hosted The Future Minerals Forum in January 2024 and gathered over 25 African governments, in an attempt to be seen as a major player in the regional and international mining sector. Saudi Arabia is placing itself in the middle of the so-called “Super Region” to connect minerals-rich countries to Gulf countries, which benefit from low-cost energy and can process raw materials and manufacture end-products, as well as to large and growing consumer markets such as India40.

The UAE, a growing presence in Africa for more than a decade

The UAE have invested in Africa over the past two decades with a primary focus on infrastructure, in particular ports through state-owned companies DP World and AD Ports, which are crucial for the trade of critical minerals. It has been the 4th financier of the continent over a decade behind China, the EU and the US, culminating with $97bn pledged in 2022 and 202341.

UAE interests in Africa have been associated with its dependency for food supply, and investments were meant to secure more resilient food supply chain (85% of the country’s food is imported42), while Africa’s growing demand for energy represented a huge potential market for Emirati industries.

Even though an investment in a bauxite mine in Guinea was completed as early as in 2013, the majority of deals related to critical minerals has been made more recently. In 2023, the Emirati company IRH paid $1.1bn for a majority stake in a copper mine (Mopani) in Zambia while the Abu Dhabi gold trader Primera Group was granted a 25-year monopoly by the DRC government for all small-scale “artisanal” gold supplies in the country, and the construction of 4 additional mines. In 2024, the UAE have been active in Angola (signature of a JV for extraction of iron ores), Burundi (advanced talks announced for a deal about nickel) and Kenya (signature of a MoU to partner on mineral exploration, mine development, mineral processing, refining and marketing).

The role of India and its massive internal market

India has an objective of becoming net zero by 2070, with an intermediate goal of 50% of electric power capacity stemming from non-fossil energies by 2030. On top of electricity generation, it also aims to decarbonize the transportation sector with a target of 80 million EVs (30% of vehicle sales) by 203043. This transition at the scale of India implies the consumption of a massive quantity of raw materials including critical minerals. The scale of the challenge led India to publish in June 2023 a list of 34 Critical Raw Materials that are key to its strategic independence in sectors like energy, defense, telecommunications, etc.

India is endowed with lithium recently discovered, cobalt, copper, nickel, but in limited quantities. In addition, it has not particularly developed its mining industry, which has created an import need for its local production, in particular regarding the solar sector and EVs. In this context, the Indian critical minerals strategy relies on two pillars:

On several occasions, Indian officials have emphasized the importance of Africa for India45, which was reiterated recently by the Foreign Affairs Minister who names Africa India’s “sister continent”46, with a particular attention brought to the construction of mutually beneficial relationships47. In 2018, Prime Minister Narendra Modi outlined 10 guiding principles for India-Africa Engagement48 which define among other that development partnerships shall be driven by Africa’s priorities to enable local development, that India’s private sector shall be encouraged to invest in Africa, and that their large markets shall be kept open to become key trade partners.

In a nutshell, India aims to offer another model of development for Africa based on greater inclusion and transparency49. India is now Africa’s third largest trading partner with India-Africa trade reaching more than $100bn in 202350, behind the EU and China and is one of the largest lenders to the continent with cumulative investments of more than $70bn51 including investments in the mining and energy sectors. Therefore, India’s strategy regarding critical minerals in Africa shall be understood as part of its broader geopolitical policy. In summer 2024, a dozen of African resource-rich countries were in discussion to secure partnerships for India’s supplies of minerals: the DRC, Ivory Coast, Madagascar, Malawi, Mali, Morocco, Mozambique, South Africa, Tanzia, Zambia, Zimbabwe 52.

Beyond bilateral agreements, New Delhi recently joined Western initiatives such as the MSP next to Western countries, and it is also in discussion to create partnerships with Western countries such as Australia. Indeed, the country is of interest to the Western world due to its vast market with industrial capabilities that can offer an alternative to China.

African perspective: how to avoid another resource curse?

African resources in the global market of critical minerals

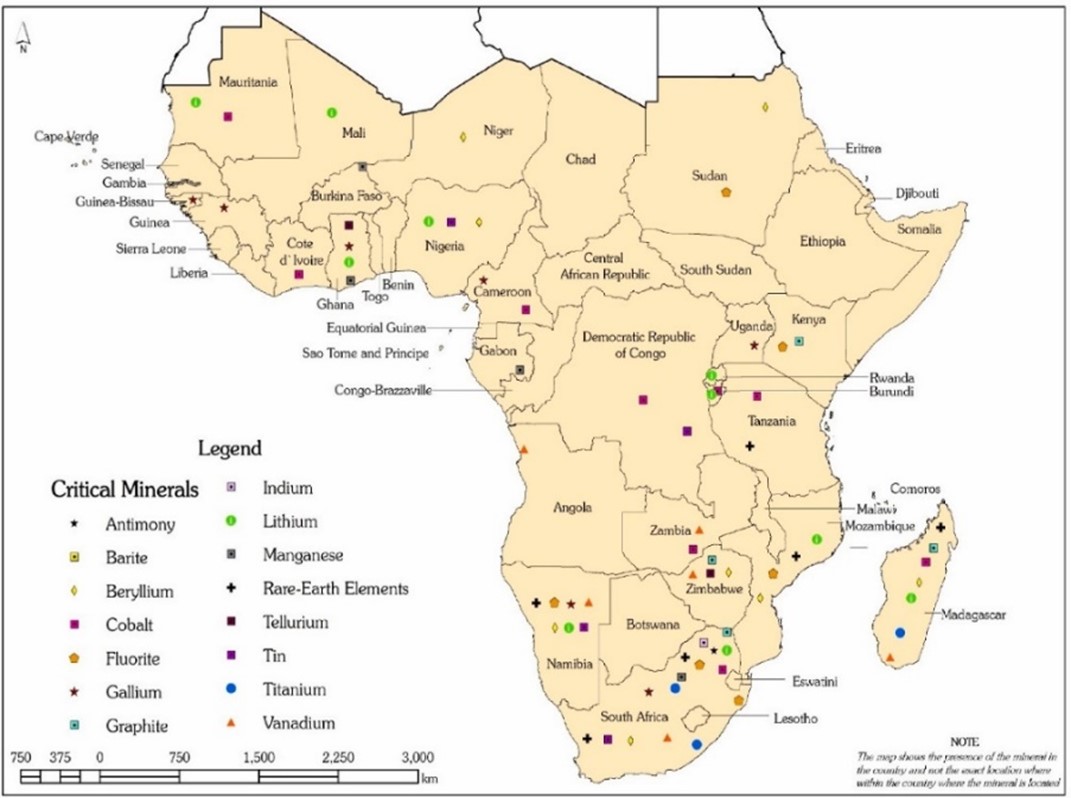

There cannot be a green future without African minerals: Sub-Saharan Africa is home to 30% of the minerals necessary to the clean transition, which can represent a great opportunity for the development of the continent53. The continent is particularly rich in cobalt with 79% of global reserves, manganese with 44% of the global reserves, graphite (21%)54, etc. In 2021, it was the world’s top producer of rhodium, platinum, cobalt, and palladium.

Figure 8 – Presence of critical minerals in sub-Saharan Africa (Source: James Boafo, Jacob Obodai, Eric Stemn and Philip Nti Nkrumah 2024 [55])

Today the DRC alone mines 3/4 of global cobalt but exports most of it unprocessed. This is just an example of a larger pattern across Africa mining industry. To benefit from the energy transition, the continent needs to develop domestical refining, processing and manufacturing of end-products capabilities. Such development faces several challenges56:

The development of extraction activities in Africa is also subject to the sensitivity of mining companies vis-à-vis short-term fluctuations of raw materials prices57. This challenge is even more important for mining projects that investment decisions can be taken based on short term price signals versus investment horizons over decades. Yet the risks associated with mining development cannot be ignored, hence the importance of combining private and public investments to guide these projects towards success.

Africa, on the verge of leveraging its natural resources?

For the past decade, China had been mainly the sole investor able to finance ambitious infrastructure projects through the BRI. However, criticisms have appeared regarding the lack of transparency of the program, the poor environmental and social standards, and the burden for the recipients’ economies of the related debts. Whereas China has reduced its investments in the context of the Covid crisis and the financial repercussions of the real estate sector difficulties in the wake of Evergrande’s collapse and has revisited its strategy to focus on smaller projects, the entry of new players to finance mining-related projects creates an opportunity for African countries.

Yet, to transform African resources into an opportunity for the economic development of the continent, the projects must bring local value. In Dec 2022, the African Development Bank released a paper “Approach paper towards preparation of an African Green Minerals Strategy” outlining how Africa should diversify from the mining activities to foster its development. The report states that to strategically use the continent’s resources, the development of the mining industry should be based on 4 pillars:

More broadly, mining-related projects developed in partnership with a foreign power should enable technology and knowledge transfer, the development of adequate energy infrastructure and systems necessary for extracting and processing activities – which could also be a source of acceleration of renewable energy deployment – and the development of related infrastructures (transportation, water, digital) which contribute to regional economic development.

Conclusion – What lessons can the EU draw to become a key partner for the African continent?

At the 2023 Berlin Energy Transition Forum, Kenyan President William Ruto emphasized that with the right level of investment and the right partnerships (i.e. which consider social and environmental issues), Africa could become one of the most important partners for Europe 58.

First of all, the EU needs to consider Africa as a strategic ally with whom to build win-win partnerships. Should the EU fail to be a partner creating added value locally, developing skills and infrastructures, respecting sustainability and responsibility criteria, and ensuring transparency and accountability vis-à-vis local communities, it might reinforce the divergence between the two continents.

Second, the EU would need to build partnerships based on its strengths and look for partners to reinforce areas of weaknesses. The EU and the European private sector have an expertise and a credibility on topics such as sustainability and responsibility, the development of infrastructure and sound governance. However, the largest mining players in the world are not European ones and the mining industry is no more a major one. Multilateral partnerships and partnerships with like-minded countries can bring all the necessary competences around the table.

Third, it should develop a consistent and credible strategy to achieve its objectives, in particular on two aspects: financing and credibility of the EU as the main interlocutor for the African continent.

Eventually, the race towards energy transition offers an opportunity to be seized: energy policy – which used to rely on fossil fuels’ supply security – could be a vector of enhanced cooperation, in particular with the African continent. Making the energy policy the central piece of cooperation between the two continents would create a much-needed convergence between climate ambitions and necessary social and economic developments.

Founding Partner & CEO

Member of the Siparex Executive Committee

Co-founder &

Managing Partner

Co-founder &

Managing Partner

Associate

Notes & references

1 Vincent Donnen, « Vers une ère métallisée : renforcer la résilience des industries par un mécanisme de stockage stratégique de métaux rares », Notes de l’Ifri, Ifri, mai 2022.

2 D.S. Abraham, The Elements of Power: Gadgets, Guns, and the Struggle for a Sustainable Future in the Rare Metal Age, New Haven: Yale University Press, 2015

3 International Monetary Fund (IMF). 2024. “Digging for Opportunity: Harnessing Sub-Saharan Africa’s Wealth in Critical Minerals.” In Regional Economic Outlook: Sub-Saharan Africa—A Tepid and Pricey Recovery. Washington, DC, April., page 2

4 IEA, “Global Critical Minerals Outlook 2024”, https://iea.blob.core.windows.net/assets/ee01701d-1d5c-4ba8-9df6-abeeac9de99a/GlobalCriticalMineralsOutlook2024.pdf

5 U.S. Geological Survey, 2024, Mineral commodity summaries 2024: U.S. Geological Survey, 212 p., https://doi.org/10.3133/mcs2024., page 145

6 Julian Kettle, Patrick Barnes and Chris Sim, 17 Jan 2024, “How can the Super Region enable the energy transition?”, Wood Mackenzie, https://www.woodmac.com/news/opinion/ebook-how-can-the-super-region-enable-the-energy-transition/

7 IEA, “Global Critical Minerals Outlook 2024”, https://iea.blob.core.windows.net/assets/ee01701d-1d5c-4ba8-9df6-abeeac9de99a/GlobalCriticalMineralsOutlook2024.pdf

8 David Pilling, 23 Aug 2024, “The foreign powers competing to win influence in Africa”, Financial Times, https://www.ft.com/content/a811400c-6c1f-4970-b1a9-4e9d28efa62e

9 Tse, Pui-Kwan, 2011, China’s rare-earth industry: U.S. Geological Survey Open-File Report 2011–1042, 11 p., page 2, https://pubs.usgs.gov/of/2011/1042/of2011-1042.pdf

10 Charles Chang, Diego Ocampo, Claire Yuan, Annie Ao, Stephen Chan, and Avery Chen, 24 Aug 2023, “China’s global reach grows behind critical minerals”, S&P Global, https://www.spglobal.com/en/research-insights/special-reports/china-s-global-reach-grows-behind-critical-minerals

11 Charles Chang, Diego Ocampo, Claire Yuan, Annie Ao, Stephen Chan, and Avery Chen, 24 Aug 2023, “China’s global reach grows behind critical minerals”, S&P Global, https://www.spglobal.com/en/research-insights/special-reports/china-s-global-reach-grows-behind-critical-minerals

12 World Economic Forum, 5 Jan 2023, https://www.weforum.org/stories/2023/01/chart-countries-produce-lithium-world/

13 Initiative « matières premières » – répondre à nos besoins fondamentaux pour assurer la croissance et créer des emplois en Europe. COM(2008) 699, page 5

14 Nedopil, Christoph, 2024, China Belt and Road Initiative (BRI) Investment Report 2023, Griffith Asia Institute, Griffith University (Brisbane) and Green Finance & Development Center, FISF Fudan University (Shanghai), page 1, DOI: 10.25904/1912/514

15 Briana Boland, Eric Olander, Lauren Herzer Risi and Tom Sheehy, 29 Jun 2023, “China’s Critical Mineral Supply Chains in Africa | How China’s Critical Mineral Supply Chains Impact Peace and Security on the Continent”, US Institute of Peace, https://www.usip.org/events/chinas-critical-mineral-supply-chains-africa (6:20)

16 Nedopil, Christoph, 2024, China Belt and Road Initiative (BRI) Investment Report 2023, Griffith Asia Institute, Griffith University (Brisbane) and Green Finance & Development Center, FISF Fudan University (Shanghai), page 6, DOI: 10.25904/1912/514/

17 Nedopil, Christoph, 2024, China Belt and Road Initiative (BRI) Investment Report 2023, Griffith Asia Institute, Griffith University (Brisbane) and Green Finance & Development Center, FISF Fudan University (Shanghai), page 5, DOI: 10.25904/1912/514/

18 Desmond Egyin, 2 May 2024, “Addressing China’s Monopoly over Africa’s Renewable Energy Minerals”, Wilson Center, https://www.wilsoncenter.org/blog-post/addressing-chinas-monopoly-over-africas-renewable-energy-minerals

19 “China’s Critical Mineral Supply Chains in Africa”, US Institute of Peace, 29 June 2023, https://www.usip.org/events/chinas-critical-mineral-supply-chains-africa

20 John Coyne and Justin Bassi, 20 Mar 2024, “China’s dominance over critical minerals poses an unacceptable risk”, Lowy Institute, https://www.lowyinstitute.org/the-interpreter/china-s-dominance-over-critical-minerals-poses-unacceptable-risk

21 IEA, “Global Critical Minerals Outlook 2024”, https://iea.blob.core.windows.net/assets/ee01701d-1d5c-4ba8-9df6-abeeac9de99a/GlobalCriticalMineralsOutlook2024.pdf

22 EIB, “Rwanda and EIB agree new Critical Raw Materials investment partnership”, 19 December 2023, https://www.eib.org/en/press/all/2023-530-rwanda-and-eib-agree-new-critical-raw-materials-investment-partnership

23 Diana-Paula Gherasim, “The Troubled Reorganization of Critical Raw Materials Value Chains: An Assessment of European De-risking Policies”, Ifri Papers, Ifri, September 2024, https://www.ifri.org/en/papers/troubled-reorganization-critical-raw-materials-value-chains-assessment-european-de-risking

24 Andres Schipani, 21 Aug 2024, “The US-backed railway sparking a battle for African copper”, Financial Times, https://www.ft.com/content/cb2823c7-f451-4bc9-959e-ec7e07384a31

25 Amy Gunia, 4 Nov 2024, “A rejuvenated railway could change how minerals move in Africa – and globally”, CNN, https://edition.cnn.com/world/africa/angola-lobito-corridor-railway-impact-spc/index.html#:~:text=Critics%20say%20that%20the%20corridor’s,developing%20local%20value%2Dadded%20processing.

26 US Department of Energy, Critical Minerals and Materials Strategy: https://www.energy.gov/sites/prod/files/2021/01/f82/DOE%20Critical%20Minerals%20and%20Materials%20Strategy_0.pdf

27 US Department of Energy, Critical Minerals and Materials Strategy: https://www.energy.gov/sites/prod/files/2021/01/f82/DOE%20Critical%20Minerals%20and%20Materials%20Strategy_0.pdf

28 Zainab Usman, 8 Feb 2024, “America should not allow its trade programme with Africa to die”, Financial Times, https://www.ft.com/content/9a758373-4c5b-40e7-859e-04e5beaa7e4f

29 Zainab Usman, 8 Feb 2024, “America should not allow its trade programme with Africa to die”, Financial Times

30 US Department of State : https://www.state.gov/2022-u-s-africa-leaders-summit-overview/#:~:text=The%20December%2013%2D15%2C%202022,billion%20in%20Africa%20through%202025.

31 Diana-Paula Gherasim, “The Troubled Reorganization of Critical Raw Materials Value Chains: An Assessment of European De-risking Policies”, Ifri Papers, Ifri, September 2024, https://www.ifri.org/en/papers/troubled-reorganization-critical-raw-materials-value-chains-assessment-european-de-risking

32 Gracelin Baskaran, 14 Nov 2024, “Seven Recommendations for the New Administration and Congress: Building U.S. Critical Minerals Security”, Center for Strategic and International Studies, https://www.csis.org/analysis/seven-recommendations-new-administration-and-congress-building-us-critical-minerals

33 Alessandra Hool, David Peck, and Patrick Wäger, 13 Nov 2024, “Possible Implications of Trump’s re-election on critical raw materials dynamics”, International Round Table on Materials Criticality, https://irtc.info/2024/11/13/possible-implications-of-trumps-re-election-on-critical-raw-materials-dynamics/

34 Vision 2030, National Industrial Development and Logistics Program Delivery Plan, https://www.vision2030.gov.sa/media/bsan2azp/2021-2025-national-industrial-development-and-logistics-program-delivery-plan-en.pdf

35 Zenger News, 28 Jan 2024, “Doubling The Critical Mineral Potential Of Saudi Arabia”, Forbes, https://www.forbes.com/sites/zengernews/2024/01/28/doubling-the-critical-mineral-potential-of-saudi-arabia/

36 Said Bakr, 20 Jun 2024, “Saudi Arabia’s and the UAE’s Quest for African Critical Minerals”, The Arab Gulf States Institute in Washington, https://agsiw.org/saudi-arabias-and-the-uaes-quest-for-african-critical-minerals/

37 “Rio Tinto, Saudi Arabia eye stake in First Quantum’s Zambia copper mines”, 19 Apr 2024, Mining Technology, https://www.mining-technology.com/news/rio-tinto-saudi-arabia-stake/

38 Gracelin Baskaran, 5 Dec 2023, “Saudi Arabia Has a Strategic Advantage in Sourcing Critical Minerals from Africa”, Center for Strategic & International Studies, https://www.csis.org/analysis/saudi-arabia-has-strategic-advantage-sourcing-critical-minerals-africa

39 Julian Kettle, Patrick Barnes and Chris Sim, 17 Jan 2024, “How can the Super Region enable the energy transition?”, Wood Mackenzie, https://www.woodmac.com/news/opinion/ebook-how-can-the-super-region-enable-the-energy-transition/

40 Julian Kettle, Patrick Barnes and Chris Sim, 17 Jan 2024, “How can the Super Region enable the energy transition?”, Wood Mackenzie, https://www.woodmac.com/news/opinion/ebook-how-can-the-super-region-enable-the-energy-transition/

41 David Pilling, Chloe Cornish and Andres Schipani, 30 May 2024, “The UAE’s rising influence in Africa”, Financial Times, https://www.ft.com/content/388e1690-223f-41a8-a5f2-0c971dbfe6f0

42 Maddalena Procopio and Corrado Cok, 20 Jun 2024, “Beyond competition, How Europe can harness the UAE’s energy ambitions in Africa”, European Council on Foreign Relations, https://ecfr.eu/publication/beyond-competition-how-europe-can-harness-the-uaes-energy-ambitions-in-africa/

43 Dhanasree Jayaram and Ramu C. M., 25 Apr 2024, “India’s critical minerals strategy: Geopolitical imperatives and energy transition goals”, Finnish Institute of International Affairs, https://www.fiia.fi/en/publication/indias-critical-minerals-strategy?read

44 Dhanasree Jayaram and Ramu C. M., 25 Apr 2024, “India’s critical minerals strategy: Geopolitical imperatives and energy transition goals”, Finnish Institute of International Affairs, https://www.fiia.fi/en/publication/indias-critical-minerals-strategy?read

45 “India sees Africa as natural partner; will be at top of our priorities: EAM”, 25 Jun 2024, Business Standard, https://www.business-standard.com/external-affairs-defence-security/news/india-sees-africa-as-natural-partner-will-be-at-top-of-our-priorities-eam-124062501300_1.html

46 Paul Nantulya, 12 Dec 2023, “Africa-India Cooperation Sets Benchmark for Partnership”, Africa Center for Strategic Studies, https://africacenter.org/spotlight/africa-india-cooperation-benchmark-partnership/

47 “India sees Africa as natural partner; will be at top of our priorities: EAM”, 25 Jun 2024, Business Standard, https://www.business-standard.com/external-affairs-defence-security/news/india-sees-africa-as-natural-partner-will-be-at-top-of-our-priorities-eam-124062501300_1.html

48 H.H.S. Viswanathan and Abhishek Mishra, June 2019, “The Ten Guiding Principles for India-Africa Engagement: Finding Coherence in India’s Africa Policy”, Observer Research Foundation, https://www.orfonline.org/public/uploads/posts/pdf/20230725183847.pdf

49 https://issafrica.org/iss-today/india-eyes-africa-in-its-quest-for-superpower-status

50 Paul Nantulya, 12 Dec 2023, “Africa-India Cooperation Sets Benchmark for Partnership”, Africa Center for Strategic Studies, https://africacenter.org/spotlight/africa-india-cooperation-benchmark-partnership/

51 Paul Nantulya, 12 Dec 2023, “Africa-India Cooperation Sets Benchmark for Partnership”, Africa Center for Strategic Studies, https://africacenter.org/spotlight/africa-india-cooperation-benchmark-partnership/

52 “India stepping up critical mineral acquisition plans with dozen African countries”, 9 Jun 2024, North Africa Post, https://northafricapost.com/77987-india-stepping-up-critical-mineral-acquisition-plans-with-dozen-african-countries.html

53 International Monetary Fund (IMF). 2024. “Digging for Opportunity: Harnessing Sub-Saharan Africa’s Wealth in Critical Minerals.” In Regional Economic Outlook: Sub-Saharan Africa—A Tepid and Pricey Recovery. Washington, DC, April

54 Julian Kettle, Patrick Barnes and Chris Sim, 17 Jan 2024, “How can the Super Region enable the energy transition?”, Wood Mackenzie, https://www.woodmac.com/news/opinion/ebook-how-can-the-super-region-enable-the-energy-transition/

55 James Boafo, Jacob Obodai, Eric Stemn and Philip Nti Nkrumah, 2024, “The race for critical minerals in Africa: A blessing or another resource curse?”, Resources Policy 93, https://doi.org/10.1016/j.resourpol.2024.105046

56 International Monetary Fund (IMF). 2024. “Digging for Opportunity: Harnessing Sub-Saharan Africa’s Wealth in Critical Minerals.” In Regional Economic Outlook: Sub-Saharan Africa—A Tepid and Pricey Recovery. Washington, DC, April

57 J. Peter Pham, 16 Mar 2024, “Analysis. The Middle East and Africa’s Strategic Minerals”, Powers of Africa, https://powersofafrica.com/article/493/analysis-the-middle-east-and-africas-strategic-minerals

58 Kenyan President William Ruto at the 2023 Berlin Energy Transition Dialogue